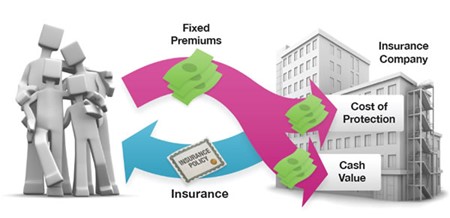

In exchange for fixed premiums, an insurance company promises to pay a set benefit when the policyholder dies, but also offers additional benefits as well. Whole life insurance policies can build up cash value — effectively a cash reserve that pays a modest rate of return, and the growth is tax-deferred. Guarantees are based on the claims-paying ability of the issuing company.

In exchange for fixed premiums, an insurance company promises to pay a set benefit when the policyholder dies, but also offers additional benefits as well. Whole life insurance policies can build up cash value — effectively a cash reserve that pays a modest rate of return, and the growth is tax-deferred. Guarantees are based on the claims-paying ability of the issuing company.

Most whole life insurance policies allow policyholders to borrow a portion of their policy’s cash value. Access to the cash value can allow you to pay for things like college expenses, a home down payment, or any other needs you may have. Interest payments on policy loans go directly back into the policy’s cash value.

Most whole life insurance policies allow policyholders to borrow a portion of their policy’s cash value. Access to the cash value can allow you to pay for things like college expenses, a home down payment, or any other needs you may have. Interest payments on policy loans go directly back into the policy’s cash value.

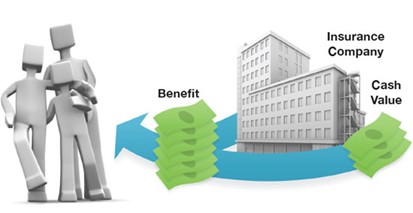

When the policyholder dies, his or her beneficiaries receive the benefit from the policy. Depending on how the policy is structured, benefits may or may not be taxable.

When the policyholder dies, his or her beneficiaries receive the benefit from the policy. Depending on how the policy is structured, benefits may or may not be taxable.

Whether whole life insurance is the best choice for you may depend on a variety of factors, including your goals or circumstances.

When you borrow against this cash value of your policy, there are some important points to consider. Accessing the cash value of the insurance policy through borrowing — or partial surrenders — has the potential to reduce the policy’s cash value and benefit. Accessing the cash value may also increase the chance that the policy will lapse and may result in a tax liability if the policy terminates before your death.

As with all types of life insurance, several factors will affect the cost and availability of whole life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder may also pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this content, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for you or your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Allos Investment Advisors®, LLC.

The content of this letter does not constitute a tax or legal opinion. Always consult with a competent professional service provider for advice on tax or legal matters specific to your situation. To the extent that a reader has any questions regarding the applicability of any specific issue discussed in this content, he/she is encouraged to consult with the professional advisor of his/her choosing.

Published for the blog on July 27, 2023 by Allos Investment Advisors®, LLC.